Ever wonder what your home is valued at? Or your neighbors? Or someone’s home that’s 6 states away? What if I told you that there is a way to find out- with just one click of a button?

That’s right, the website Ownerly.com can find the value of your home and more. Let’s dive in to what Ownerly is, the pros and cons of using it, other alternatives, and if it is right for you.

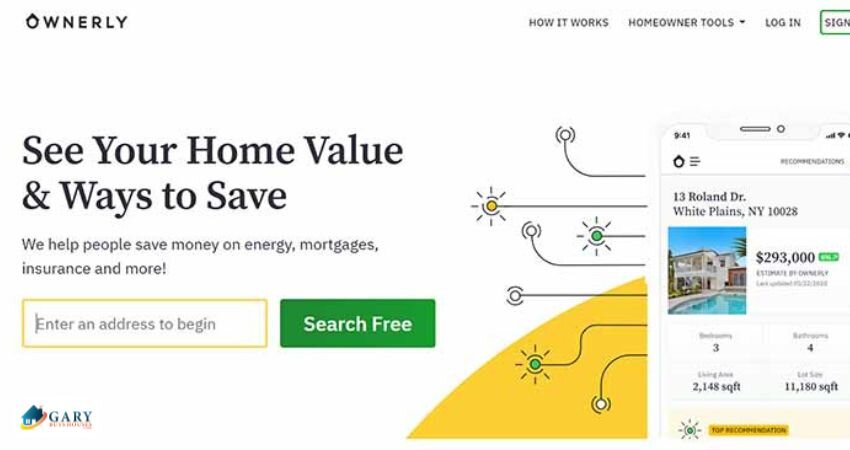

What is Ownerly?

Ownerly is an online website that searches and finds the value of your home, and any address you type in. If your curious about your local housing market, Ownerly may be a good option for you. Ownerly was founded in 2018 in New York, and currently is only available for people living in the United States.

Ownerly has access to data such as mortgage rates, home owners insurance options, loan providers, utility and energy offers, and more. On one hand, it can be a great tool to find out the value of a home, whether you are looking at buying, selling, or if you just want to know.

On the other hand, it is still a new company, the reviews for it are mixed, and there aren’t as many features as other home valuation options out there. Let’s look a little bit more about Ownerly and then discuss the pros and cons to using it.

How does Ownerly work?

When you get on to Ownerly.com there is a search bar that will prompt you to enter in an address. Ownerly can then pull up the value and other needed information about said address. You will need to create an account to use that feature, and it is a paid service, which we will cover in a moment. For a 7 day trial however, it will only cost you $1 and give you up to 25 address reports during that trial period.

Also on their website Ownerly has an extensive blog about housing market topics that you can check out, as well as other features that might be helpful to look at. (Many of the other features Ownerly offers can be found with a Google search, but Ownerly consolidates the information and puts it in one place that is easy to access and understand.)

How much does Ownerly cost?

If you are looking in to Ownerly and only want to try it out for a few days, you have two options. First, the $1 option. For a 7 day trial you only pay $1 and get access to view 25 housing reports. If instead, you pay $5 for the trial, you get 25 housing reports that you can download and print for 7 days.

After the trial ends the billing plan is $29.99 plus tax per month, for 25 reports per month to view and download. If you like Ownerly and think you will use it a lot the monthly subscription might be nice. The average person shouldn’t need to look up 25 housing reports per month, so if you decide it’s not for you make sure to cancel it before your trial period runs out.

Ownerly for buyers

The housing market is currently slower than the past few years, and it can be hard to know what is a fair price and what your should be paying. Ownerly can be a good way to find out what value is placed on different houses.

Some reviews on Ownerly have high marks. However, others, such as these reviews found on Trustpilot don’t give as high of marks with Ownerly. The valuations that Ownerly puts out match up with other valuation websites, for the most part. (If not a compete match, they are in the ballpark.) Ownerly.com is a clean website that presents easy to understand data and various tools that can help you in your house hunting. You may not get the exact results from Ownerly, but they are not a scam and they can give you information about the value of a home that will point you in the right direction.

Ownerly for sellers

Ownerly can also be very effective for sellers as a way to compare to houses around you, and what Ownerly prices your house’s value at. Ownerly uses an automated valuation model (AVM for short) to track and analyze its data. That means that the process of finding an estimate for a house value is machine run and using an algorithm. That is why the estimate can come so quickly. Ownerly (and other AVM tools) use public data and user data to find out the size of the property, its previous sales history, what price other local houses are selling for and more.

While Ownerly can be a great tool for finding an estimate on a house (for buyers or sellers,) there is something to be said of the benefits of a full appraisal.

Pros and cons to using Ownerly

| Pros: | Cons: |

| • Fast and easy to use • Cheap trial • Data is user friendly and easy to understand • Let’s you look up multiple addresses • Works with any address in USA | • Expensive for monthly subscription • AVM data is not always reliable • New company, things are still being updated • Website only, not mobile app • Mixed reviews |

Other alternatives to Ownerly

As well as using Ownerly there are some other things you can do to learn the value of your home.

Some other cheap or free websites that offer AVM estimates on home value include Realtor.com, Homie, or Zillow.

Beware, AVM estimates can’t tell you everything. They can’t tell you if a house needs repairs, or if it was recently renovated or added on to, any specifics about the location or the street that the house is on, zoning laws, local facts, etc. An AVM website, like Ownerly, can be a good place to start, but many people choose to hire a licensed appraiser, a broker, or a real estate agent.

While these options give you more detailed and personalized information about how much your home is worth, the downside is that they may have pricey service fees.

Another great option would be to contact Gary from Garybuyshouses.com. He will come look at your house for free and give you a cash offer in 5 days or less. It is a hassle free and easy process to not only find out the exact value of your home (in any condition,) but also give you a reliable and trusted home selling experience.